Understanding The Escalation Clause In Insurance: A Comprehensive Guide

In the ever-changing world of insurance, an escalation clause plays a crucial role in safeguarding both insurers and policyholders against inflation and rising costs. This clause ensures that coverage remains relevant and effective over time, adapting to economic fluctuations. Whether you're a business owner or an individual looking to protect your assets, understanding how escalation clauses work is essential for making informed decisions.

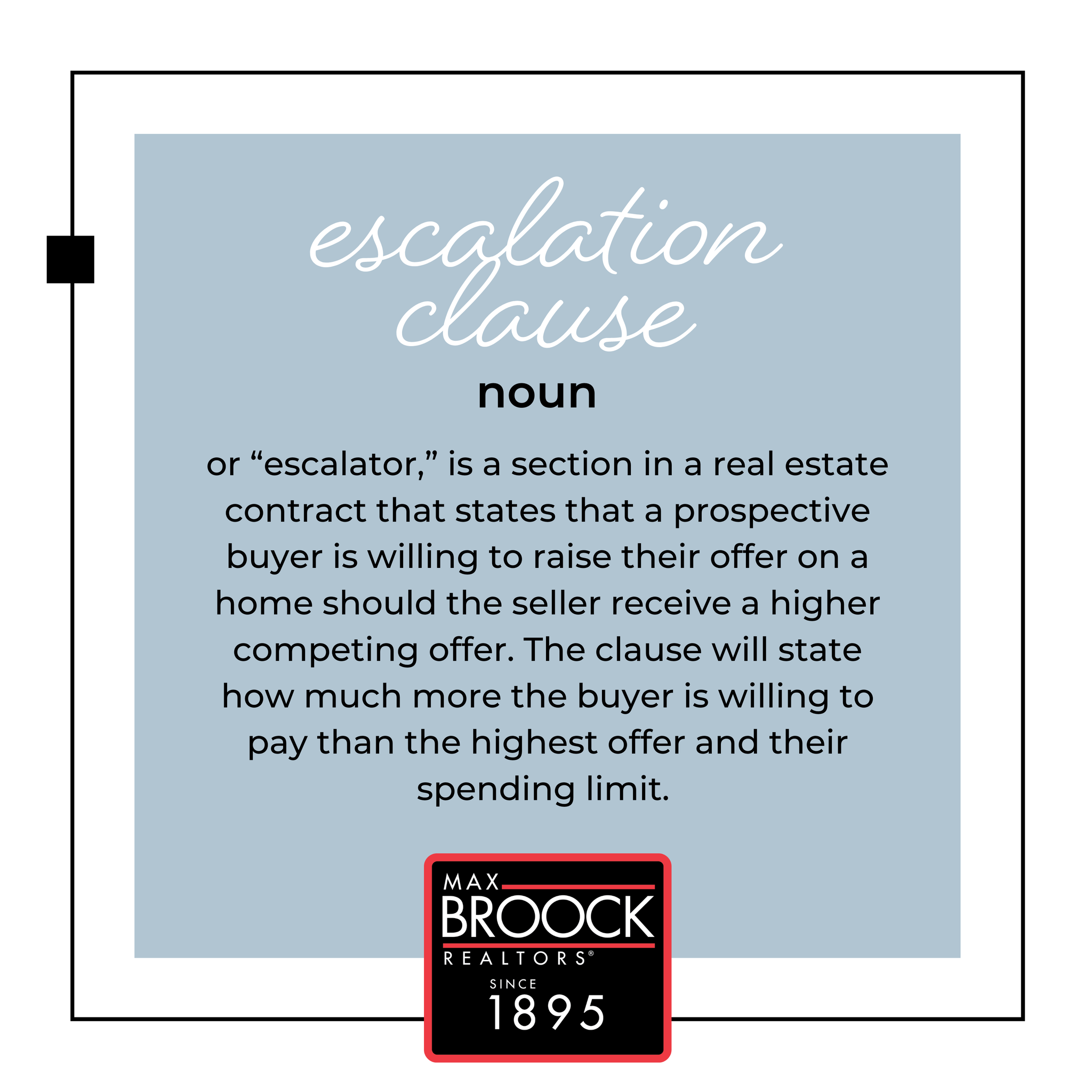

An escalation clause in insurance refers to a provision that allows for automatic adjustments in policy limits or premiums based on predefined conditions. These conditions typically revolve around inflation rates, changes in market prices, or other economic indicators. By incorporating this clause into their policies, insurers provide policyholders with peace of mind, knowing that their coverage will grow proportionally with the cost of living.

As we delve deeper into this topic, we'll explore the intricacies of escalation clauses, their benefits, and how they impact various types of insurance policies. By the end of this article, you'll have a clear understanding of why this clause is vital and how it can enhance your insurance portfolio.

Read also:Palace Wedding Cake The Ultimate Guide To Royalinspired Wedding Cakes

Table of Contents

- What is an Escalation Clause in Insurance?

- Why is an Escalation Clause Important?

- Types of Escalation Clauses

- How Does an Escalation Clause Work?

- Benefits of Including an Escalation Clause

- Challenges and Considerations

- Escalation Clause in Different Types of Insurance

- Real-World Examples of Escalation Clauses

- Legal Aspects and Compliance

- Future Trends in Escalation Clauses

What is an Escalation Clause in Insurance?

An escalation clause in insurance is a provision that allows for automatic adjustments to policy limits or premiums based on predefined conditions. These conditions usually involve economic indicators such as inflation rates, cost of living adjustments, or market price fluctuations. This clause ensures that the insured remains adequately covered as the value of their assets or liabilities increases over time.

The primary purpose of an escalation clause is to protect policyholders from the eroding effects of inflation. For example, a homeowner's policy with an escalation clause will adjust the coverage limit to account for rising construction costs, ensuring that the insured can rebuild their home at current market prices if necessary.

Key Features of an Escalation Clause

- Automatic adjustments based on predefined metrics

- Protection against inflation and rising costs

- Applicability to various types of insurance policies

Why is an Escalation Clause Important?

Inflation is a natural part of any economy, and its impact can significantly reduce the effectiveness of insurance coverage over time. Without an escalation clause, policyholders may find themselves underinsured when it comes time to file a claim. This can lead to financial strain, especially in situations where rebuilding or replacing assets is necessary.

By incorporating an escalation clause into their policies, insurers help policyholders maintain adequate coverage without the need for frequent policy reviews or adjustments. This not only benefits the insured but also simplifies the renewal process for insurance providers.

Impact on Policyholders

- Ensures coverage keeps pace with inflation

- Reduces the risk of being underinsured

- Provides peace of mind and financial security

Types of Escalation Clauses

Escalation clauses can vary depending on the type of insurance policy and the specific needs of the insured. Below are some common types of escalation clauses:

- Inflation Guard Clause: Automatically adjusts coverage limits based on inflation rates.

- Cost of Living Adjustment (COLA): Aligns coverage with changes in the cost of living.

- Indexed Escalation Clause: Links coverage adjustments to specific economic indices, such as the Consumer Price Index (CPI).

Each type of escalation clause is designed to address specific risks and ensure that coverage remains relevant and effective.

Read also:Discover The Ultimate Guide To Marley House Your Dream Destination

How Does an Escalation Clause Work?

The functioning of an escalation clause is straightforward yet sophisticated. At its core, the clause uses predefined metrics to calculate adjustments to policy limits or premiums. These metrics may include:

- Inflation rates

- Market price indices

- Construction cost indices

For instance, if the inflation rate for a given year is 3%, the policy limit will increase by 3% to reflect the rising cost of living. This ensures that the insured remains adequately covered without the need for manual adjustments.

Steps in the Adjustment Process

- Identify the relevant economic indicator (e.g., inflation rate).

- Calculate the percentage change in the indicator.

- Apply the percentage change to the policy limit or premium.

- Notify the insured of the adjustment.

Benefits of Including an Escalation Clause

Including an escalation clause in an insurance policy offers numerous advantages for both policyholders and insurers:

- Protection Against Inflation: Ensures coverage remains relevant despite rising costs.

- Simplified Renewal Process: Reduces the need for manual adjustments and policy reviews.

- Enhanced Customer Satisfaction: Provides peace of mind and financial security to policyholders.

- Improved Risk Management: Helps insurers better manage risks associated with inflation and economic fluctuations.

These benefits make escalation clauses a valuable addition to any insurance policy, particularly in volatile economic environments.

Challenges and Considerations

While escalation clauses offer significant advantages, they also come with certain challenges and considerations:

- Premium Increases: As coverage limits increase, so too may premiums, potentially impacting affordability.

- Complexity: Understanding how escalation clauses work and their impact on coverage can be challenging for some policyholders.

- Market Volatility: Rapid changes in economic indicators may lead to significant adjustments, requiring careful monitoring and management.

Insurers must carefully balance the benefits and challenges of escalation clauses to ensure they remain a viable option for policyholders.

Escalation Clause in Different Types of Insurance

Escalation clauses can be applied to various types of insurance policies, each with its own unique considerations:

Homeowners Insurance

In homeowners insurance, escalation clauses help protect policyholders against rising construction costs. This ensures that policyholders can rebuild their homes at current market prices in the event of a total loss.

Business Insurance

For businesses, escalation clauses can be crucial in maintaining adequate coverage for inventory, equipment, and other assets. This helps mitigate the financial impact of inflation on business operations.

Health Insurance

While less common, escalation clauses in health insurance can help adjust coverage limits to account for rising medical costs. This ensures that policyholders remain adequately covered for healthcare expenses.

Real-World Examples of Escalation Clauses

To better understand the practical application of escalation clauses, consider the following examples:

- A homeowner with an escalation clause in their policy sees their coverage limit increase by 3% annually to match inflation rates.

- A business owner with an indexed escalation clause adjusts their policy limits based on changes in the Producer Price Index (PPI).

- An individual with a health insurance policy incorporating a cost of living adjustment (COLA) experiences automatic increases in coverage limits to account for rising healthcare costs.

These examples illustrate how escalation clauses provide tangible benefits in real-world scenarios.

Legal Aspects and Compliance

When incorporating escalation clauses into insurance policies, insurers must adhere to relevant legal and regulatory requirements. These may include:

- Disclosure obligations: Clearly communicating the terms and conditions of the escalation clause to policyholders.

- Compliance with local regulations: Ensuring that the clause aligns with applicable laws and regulations.

- Transparency: Providing policyholders with detailed information about how adjustments are calculated and applied.

By following these guidelines, insurers can ensure that their escalation clauses are legally sound and compliant with industry standards.

Future Trends in Escalation Clauses

As the insurance industry continues to evolve, we can expect to see new trends and innovations in the use of escalation clauses:

- Advanced Analytics: Insurers may leverage big data and machine learning to refine the calculation of adjustments, making them more accurate and personalized.

- Customizable Clauses: Policyholders may have more options to tailor escalation clauses to their specific needs and risk profiles.

- Increased Adoption: As awareness of the benefits of escalation clauses grows, we can expect to see wider adoption across various types of insurance policies.

These trends highlight the potential for escalation clauses to play an even more significant role in the future of insurance.

Conclusion

In conclusion, an escalation clause in insurance is a vital tool for protecting policyholders against the eroding effects of inflation and rising costs. By automatically adjusting coverage limits and premiums based on predefined metrics, escalation clauses ensure that coverage remains relevant and effective over time. Understanding how these clauses work and their benefits can help policyholders make informed decisions about their insurance needs.

We encourage you to explore the options available in your insurance policies and consider the inclusion of an escalation clause to enhance your coverage. Don't hesitate to leave a comment or share this article with others who may find it useful. For more information on insurance and related topics, be sure to check out our other articles on the site.

{kind=link}